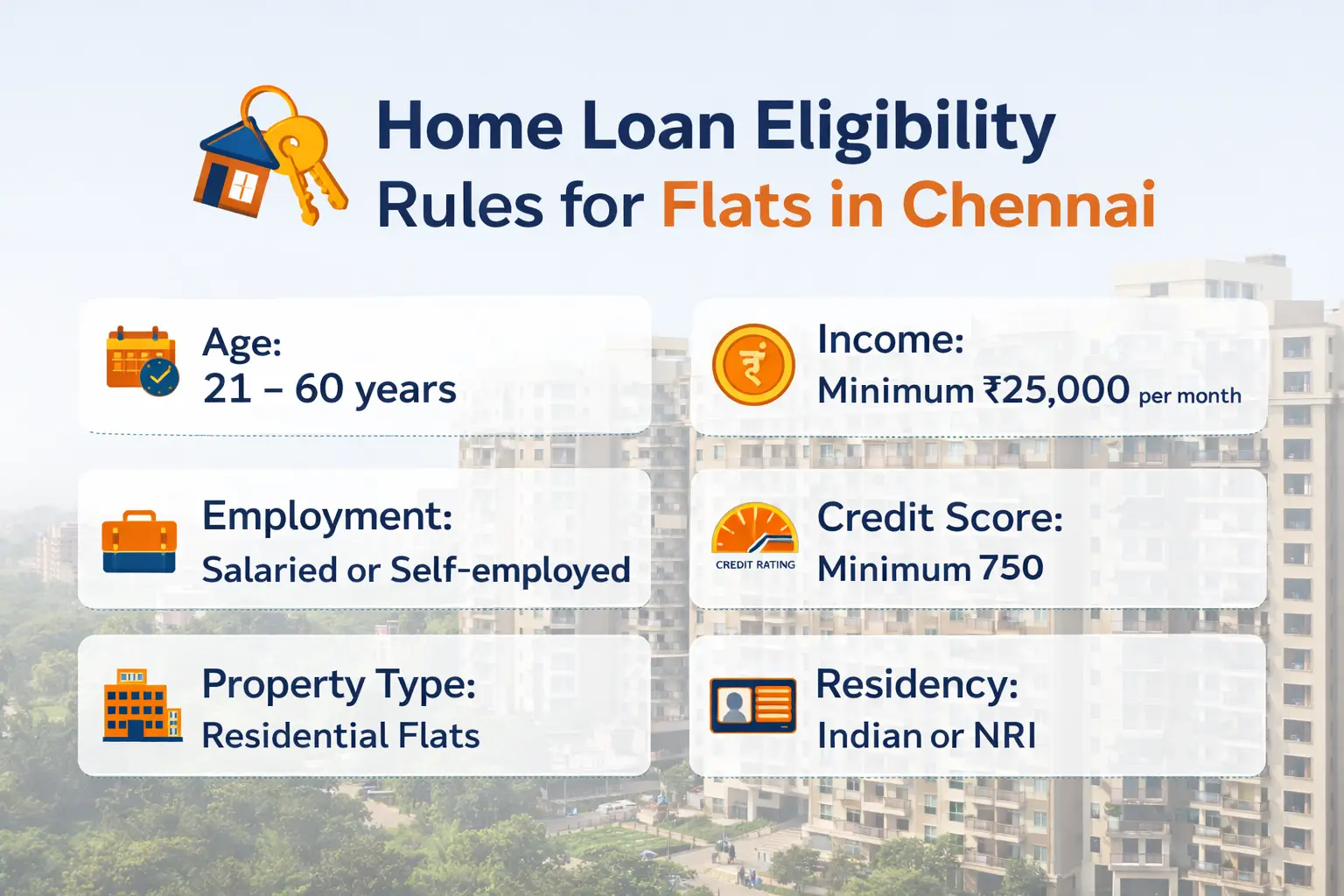

1. Who Can Apply for a Home Loan in Chennai?

Banks and Housing Finance Companies (HFCs) in India (regulated by Reserve Bank of India) allow the following applicants:

Eligible Applicants

- Salaried individuals (private, government, PSU)

- Self-employed professionals (CA, Doctor, Architect, Lawyer, etc.)

- Self-employed business owners

- NRIs / OCIs (with conditions)

- Co-applicants (spouse, earning parents)

Age Criteria

- Minimum: 21 years

- Maximum at loan maturity:

- Salaried: 60–65 years

- Self-employed: 65–70 years

2. Income Eligibility (Most Important Factor)

Banks calculate eligibility using FOIR (Fixed Obligation to Income Ratio).

General Rules

- EMI should not exceed 40–55% of net monthly income

- Higher income = higher loan eligibility

Chennai Income Benchmarks (Indicative)

Monthly Net Income

- Rs 30,000

- Rs 50,000

- Rs 75,000

- Rs 100,000+

Approx. Loan Eligibility

- Rs 20 - 25 L

- Rs 35 - 45 L

- Rs 55 - 70L

- Rs 80L - Rs 1.2cr

(Assuming 20–30 years tenure and current interest rates)

Banks like State Bank of India and HDFC Ltd follow similar income logic, though private banks may allow higher FOIR.

3. Credit Score (CIBIL Score)

Minimum Requirements

- 750+ → Best interest rates & faster approval

- 700–749 → Loan possible with slightly higher rates

- 650–699 → Reduced loan amount or co-applicant needed

- Below 650 → High rejection risk

Late payments, credit card overuse, or personal loans reduce eligibility.

4. Property Eligibility Rules for Flats in Chennai

Even if you are eligible, the flat must also be eligible.

Approved Property Criteria

- CMDA / DTCP approved layout

- Clear parent documents (minimum 30 years preferred)

- No encroachment on OSR land, water bodies, or poramboke

- Proper UDS (Undivided Share of Land)

- Completion Certificate (for ready flats)

- Approved building plan

Location Sensitivity in Chennai

Extra scrutiny for:

- Pallikaranai marshland areas

- Velachery low-lying zones

- Parts of Perumbakkam & Medavakkam

- Areas near Buckingham Canal / Cooum / Adyar river

5. Flat Type Eligibility

Ready-to-Move Flats

- Highest approval chances

- Immediate disbursement

Under-Construction Flats

- Builder must be bank-approved

- Stage-wise disbursement

- Possession date should be realistic

Resale Flats

- Property age usually ≤25–30 years

- Remaining life of building matters

- Strong legal verification required

6. Loan-to-Value (LTV) Ratio

As per RBI rules:

Property Value

- Up to 30L

- Rs 30 - 75L

- Above Rs 75L

Max Loan Allowed

- 90%

- 80%

- 75%

Example:

- Flat price Rs 80 lakhs → Max loan ≈ Rs 60 lakhs

- You must arrange the rest as down payment + registration costs

7. Employment Stability Rules

Salaried Applicants

- Minimum 2 years total experience

- At least 6–12 months in current job

- IT, Manufacturing, Banking, PSU jobs preferred in Chennai

Self-Employed Applicants

- Minimum 3 years business vintage

- Stable ITR income for last 2–3 years

- GST returns (if applicable)

8. Documentation Required

Personal Documents

- PAN, Aadhaar

- Address proof

- Passport (for NRIs)

Income Proof

Salaried

- Last 3–6 months payslips

- Form 16

- Bank statements (6 months)

Self-Employed

- ITR (2–3 years)

- Balance Sheet & P&L

- Business proof

Property Documents

- Sale Agreement

- Approved plan

- EC (Encumbrance Certificate)

- Patta / Chitta / TSLR

- Completion Certificate (if applicable)

9. Interest Rates (Chennai—Indicative)

- Public sector banks: 8.5%–9.5%

- Private banks: 9%–10.5%

- NBFCs: 10%–12%

Rates depend on:

- Credit score

- Employer profile

- Loan amount

- Property type

10. Common Reasons for Rejection in Chennai

- Flat built on unapproved land

- Missing UDS or OSR violations

- Low credit score

- Over-leveraged applicant

- Builder blacklisted by banks

- Flood-prone area risk

11. Smart Tips to Improve Eligibility

- Add earning spouse as co-applicant

- Close personal loans before applying

- Choose longer tenure (initially)

- Ensure property legal check before paying advance

- Compare banks, not just interest rates

Conclusion

In Chennai, property legality is as important as your income. Many loan rejections happen due to flat approval issues, not applicant issues.