What are some first-time homebuyer tips?

1.Start Saving Early:

Getting a mortgage requires you to put skin in the game by making a down payment on your home. That’s typically from 3% of the purchase price to 10-20%, depending on the loan.

Start saving by slashing expenses and creating a budget to help you reach your goal. You also could ask family members if they can help out. Additionally, some government programs help first-time buyers with down payments.

2.CHECK FOR BANK-APPROVALS:

An important aspect to consider while buying a house would be to check if the project is approved by a reputed bank or not. Since the bank itself verifies everything, these projects always have the assurance of being legally and financially compliant.

3.Verify through RERA Registrations:

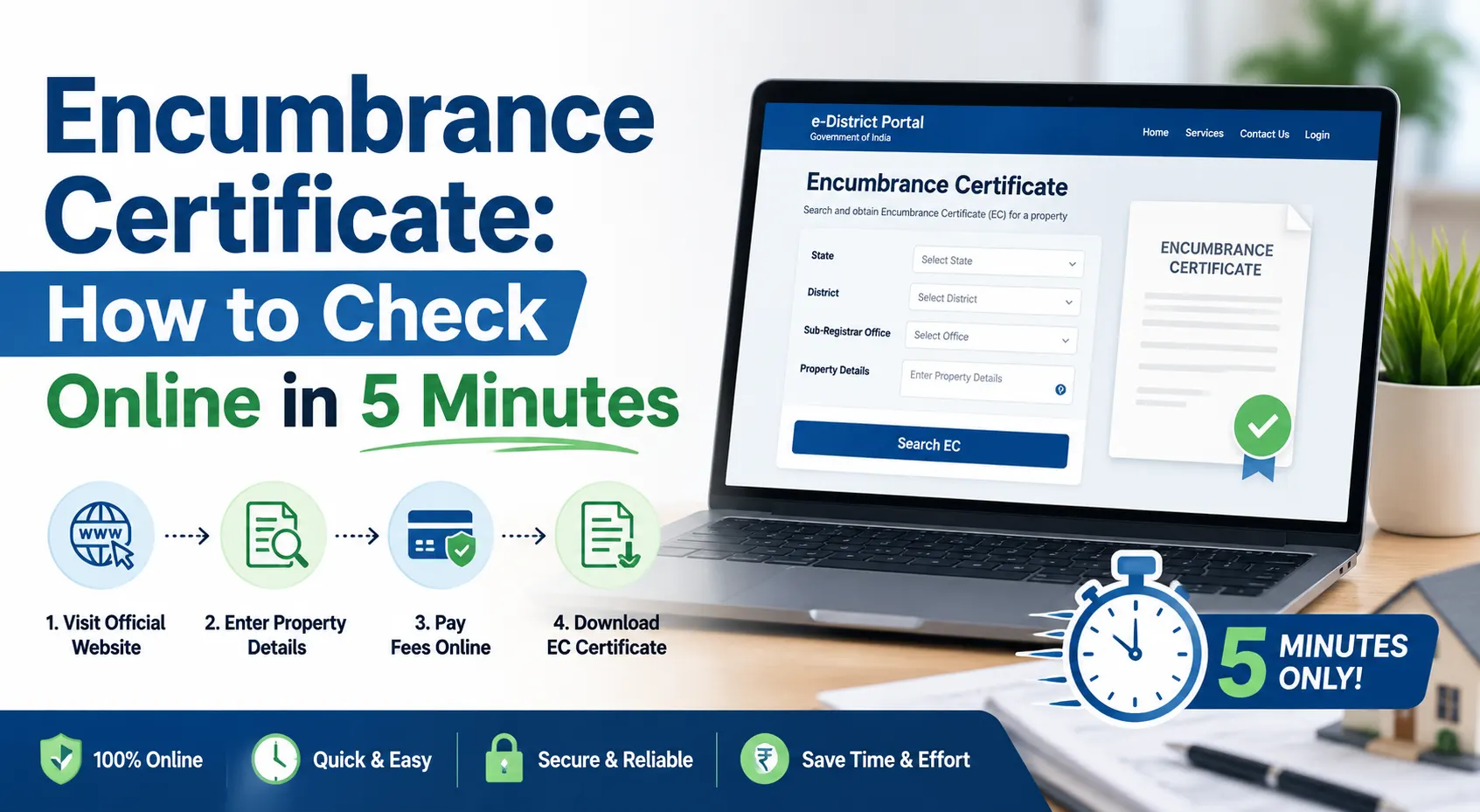

Check if the property is registered under RERA (Real Estate Regulatory Authority) and verify the RERA number online by visiting the official website.

4.Start Working on Your Credit Score as Soon as Possible:

Your credit score plays a role in getting a mortgage. Almost everyone has room for improvement. Start by paying off or paying down credit cards: the higher your available credit and the lower your utilization, the higher your score. Three to six months before you reach out to a lender, review your credit reports from all three major agencies: Equifax, Experian and TransUnion. Each will show different credit history items. You’re entitled to an annual free report from each agency, available from AnnualCreditReport.com. Look for errors such as old debts you’ve paid off or items that aren’t yours. Take steps to dispute errors, and follow up to make sure they’ve been corrected. Challenges to reports take time to resolve.

5.Consider Amenities and Specifications:

Once you’ve decided on the type of property, you need to further take into account the kind of lifestyle you wish to live; here’s where the amenities and specifications offered by the property come into play.

6.Try Not to Finance Anything New Before Buying a Home:

How much you owe will affect how much you can borrow. Financing a large new purchase before you get a mortgage (a new car, for example) reduces your loanable amount. You also may negatively impact your credit score with a large purchase, since you’re increasing utilization and lowering your available credit. That could have a bearing on home loan terms, such as interest rate. It’s best to stay away from other major purchases when you’re about to make the biggest purchase of your life.

7.Note about Maintenance Costs:

Another important factor to consider, especially if the project has a range of amenities and features. Asking about the annual maintenance costs in advance helps you gauge the total cost of living in a particular project as well.

8.Look for the Elevation of the Property:

Next up, you can ask for a drone shot of the view from your possible new home. It can even help you narrow down on the floor of the house, the balcony view, and check for ventilation and natural light.

9.Check for Vastu Compliant:

Although the belief may vary from person to person, most homebuyers do take the Vastu compliance of the residences into consideration. Therefore, most real estate developers make sure that the homes they build are Vastu-compliant. You can check for this aspect too while buying your home.

10.Consider for Noise Canceling features:

While it’s commonly perceived that a top floor apartment gets rid of the noise outside, it is not always the case. If the property is parallel to the main road, the sound of the blaring horns and commotion may reach your house. Therefore, check if the developer is providing you with sound-proof windows that cancel the outside noise to a great extent. Your home, after all, needs to be your safe and peaceful sanctuary, away from the bustling city life.

11.Look for Social Considerations:

Next, check for the social infrastructure and connectivity across the city. Make sure you buy a property that is well-connected city-wide and one where you can find the best of healthcare and education in the vicinity.

12.Suggestions for NRIs to look for Property:

If you are a non-resident Indian (NRI) and are looking to purchase a property in India for the first time, there are certain additional considerations you would need to take care of, besides the above points. You can take a look at our guide at the NRI Zone of Mahindra Lifespaces, and find everything you need to know in this regard.

13.Compare Mortgage Lenders:

It’s good to ask family and friends for recommendations but important to choose your own lender. Know what you’re looking for: best interest rates only? A loan officer to work closely with you? Contact Livehomes.in in Chennai who can deliver the best loan terms plans, interest rates, and service for your money. Livehomes.in have more Trusted Builder Projects with us and many Banking links who can help you out with Loan Terms.

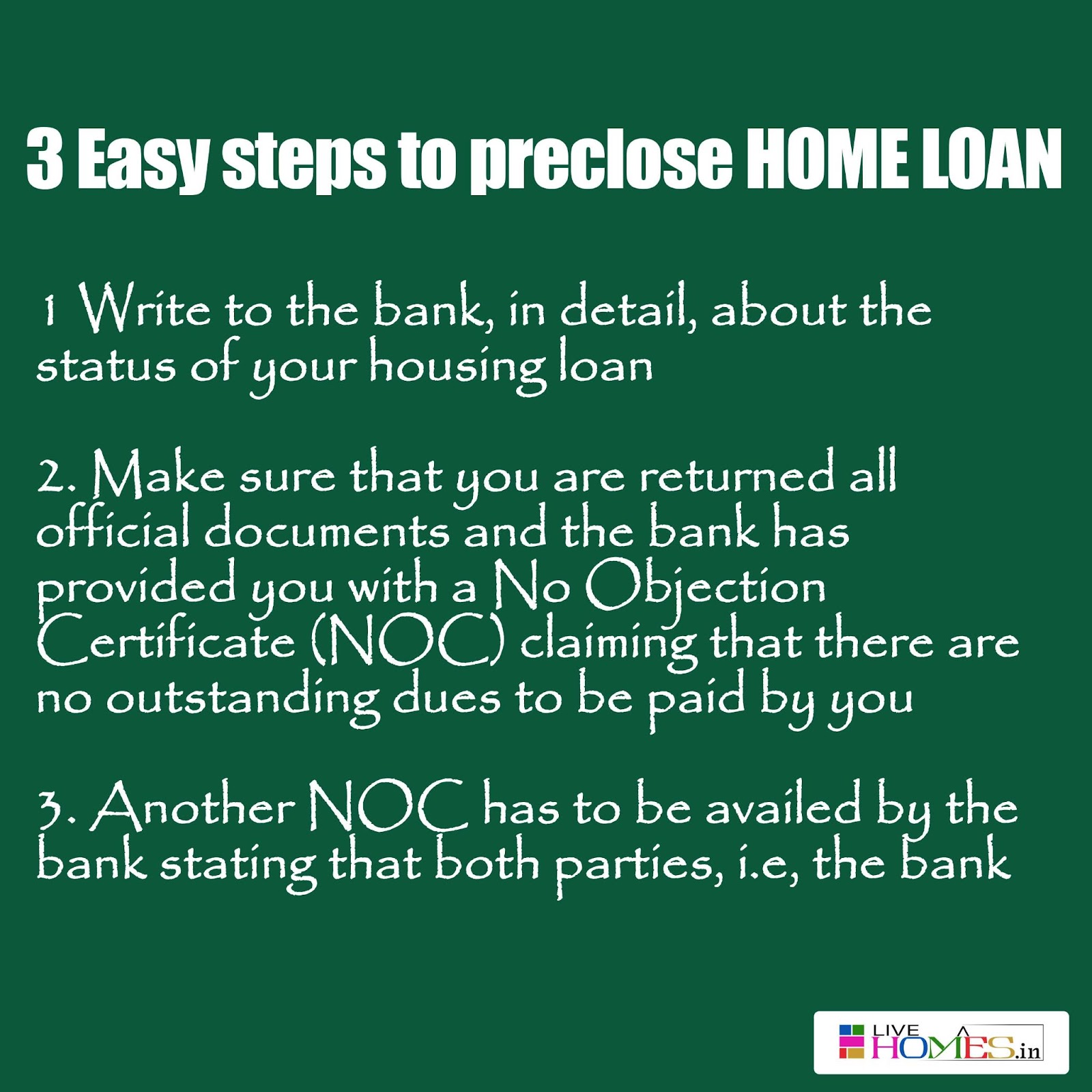

14.Get knowledge about Preclosure also:

When you’re estimating how far your cash will go toward buying a home, make sure you add in closing costs. Closing or “going to settlement” is nothing but “Pre Closure” the end of the home-buying process. That’s the day money changes hands to complete the sale. Your lender will give you an estimate of all costs early on, but many people are surprised by how much Pre closure are.

Most of the banks now a days are offering from Nil Percentage to 2% or 5%.

15. Keep an Eye Out for Other Expenses:

Your down payment and closing costs aren’t the only expenses of the mortgage process! You’ll have loan fees required by the lender, such as an appraisal fee to evaluate the property’s value and other fees; a title search fee, to make sure the seller has legal title to the property; and sometimes up-front money to prepay property insurance and taxes.

LOOKING FOR READY TO OCCUPY HOME IN CHENNAI

Make Sure for yourself before you are getting into Home Loan

Most mortgages take at least 30 days to close. Having a mortgage can be as much as a 30-year commitment.

Ask yourself a few questions below?

Are my finances in order? (Good credit, no/low debt, enough cash flow to meet monthly expenses)

Have I saved enough for a down payment and closing costs?

Can I qualify for mortgage payments that will comfortably fit my monthly budget?

Is my income stable enough to afford a mortgage, property taxes and insurance, and other expenses?

Will a home that I can afford now suit my/my family’s needs for the foreseeable future?

Do I plan to stay in the home for at least five years? (If you sell too soon, you may lose money because of the costs of buying and selling, as well as the short-term unpredictability of housing market growth.)

Looking for Exclusive and Premium Projects in Chennai Visit this Trusted Builder’s Property Site

Book your Dream Home…..

How Can We Locate A Trustworthy Real Estate Agent?

As a prospective home buyer, you might think it’s simple enough to search for homes online, but a good To Continue...