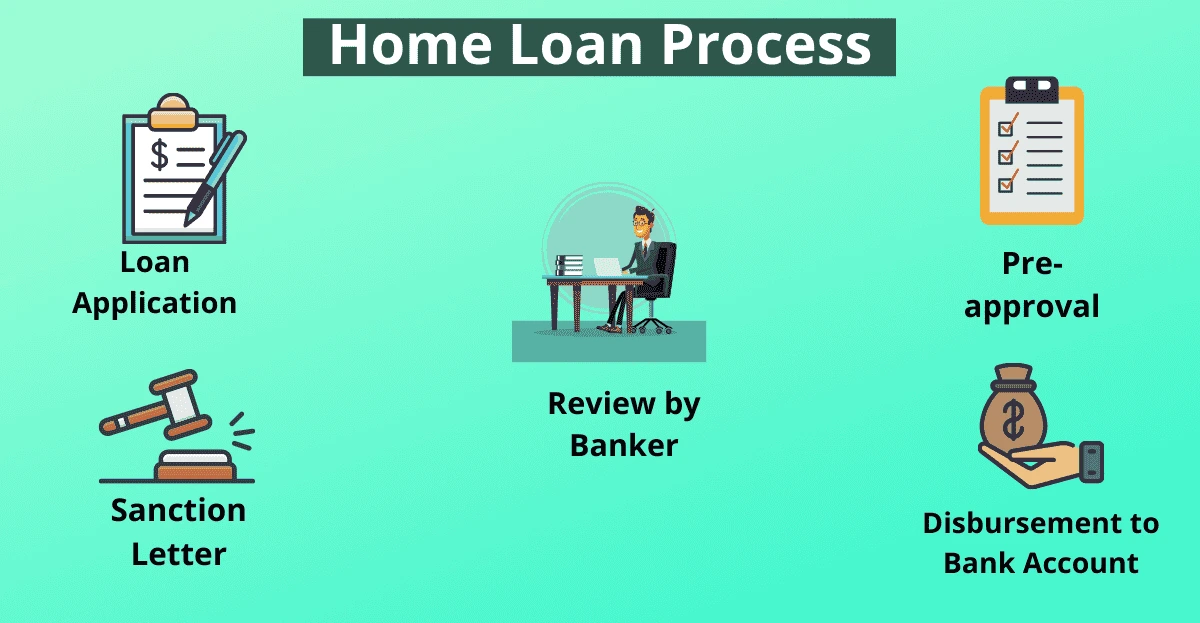

The home loan process is a series of steps that guide you from your initial loan application all the way to closing on your new home. Here's a breakdown of the typical process from start to finish:

1. Prepare for the Application

-

Check Your Credit Score: Lenders will check your credit score to determine your eligibility and the interest rate you’ll receive. It’s good to know where you stand before applying.

-

Save for a Down Payment: Most loans require a down payment (usually between 3% and 20% of the home’s purchase price). The more you can put down, the better your loan terms may be.

-

Gather Financial Documents: Lenders will ask for documents like pay stubs, tax returns, bank statements, proof of assets, and details of your current debts.

2. Get Pre-Approved for a Loan

-

Pre-Approval vs. Pre-Qualification: Pre-qualification is a general estimate of how much you can borrow based on your financial situation. Pre-approval is a more formal process where the lender verifies your financial documents and gives you a letter stating the amount they are willing to lend.

-

Choose a Lender: Research and compare different lenders, including banks, credit unions, and online lenders, to find the best rates and terms for your situation.

-

Submit Your Documents: Once you’ve selected a lender, submit all necessary financial documents for verification. This step can take a few days or more.

3. House Shopping and Making an Offer

-

Work with a Real Estate Agent: Your agent will help you find homes within your price range and assist you in making an offer.

-

Make an Offer: Once you find a home you want, make an offer. This offer may be negotiated with the seller.

-

Sign the Purchase Agreement: After agreeing on the price, both parties sign the purchase agreement, and you move on to securing the loan.

4. Formal Loan Application

-

Complete the Application: Even if you're pre-approved, you'll need to complete a formal application with the lender once you have a property in mind.

-

Loan Estimate: The lender provides a Loan Estimate (LE), which details the loan amount, interest rate, monthly payments, and closing costs.

5. Loan Processing

-

Submit Final Documentation: After your application is submitted, you'll need to provide any additional documents requested by the lender. These may include updated bank statements, proof of employment, etc.

-

Processing and Underwriting: The loan processor reviews your application and all supporting documents. The underwriter then assesses the risk of lending to you based on factors like your credit history, income, and debt-to-income ratio.

| "Best Builder Floor Apartment in Chennai" |

6. Appraisal and Inspection

-

Home Appraisal: The lender orders an appraisal to determine the market value of the home. This protects the lender by ensuring the home is worth the loan amount.

-

Home Inspection: While not required by the lender, a home inspection is a good idea to check for any major issues or needed repairs. Depending on the results, you may renegotiate with the seller or walk away from the deal.

7. Loan Approval (Clear to Close)

-

Underwriting Approval: Once the underwriter reviews all the necessary documents, they either approve the loan or request further documentation.

-

Conditional Approval: In some cases, the lender may give you conditional approval, asking for additional information or clarifications before issuing the final approval.

-

Clear to Close: If everything is in order, the lender will issue a “clear to close,” meaning you're ready for closing.

8. Closing Day

-

Final Walkthrough: Before closing, do a final walkthrough of the property to ensure everything is in the agreed-upon condition.

-

Review and Sign Documents: At closing, you’ll meet with the seller, your agent, and possibly your lender to sign the final loan documents, including the mortgage note and deed of trust.

-

Pay Closing Costs: You’ll need to pay the closing costs, which include fees for the appraisal, title search, insurance, and recording fees. These can range from 2% to 5% of the loan amount.

-

Transfer of Ownership: After signing, you’ll officially become the owner of the home, and the funds will be transferred to the seller.

9. Post-Closing

- Loan Servicing: After closing, your loan will be serviced by the lender or a third party. You will start making monthly mortgage payments according to the terms of your loan.

Each of these steps can vary depending on the type of loan, the lender, and your personal situation, but this is the general flow of the home loan process.

Read also: What is Private Mortgage Insurance PMI

https://www.livehomes.in/blogs