Buying a home is one of the biggest financial decisions most people make, and choosing the right home loan interest type can save—or cost—you lakhs over the loan tenure. In 2026, with changing RBI policies, inflation trends, and bank competition, understanding the difference between floating interest rate and fixed interest rate home loans is more important than ever.

What Is a Home Loan Interest Rate?

A home loan interest rate is the percentage charged by a bank or housing finance company on the borrowed amount.

There are mainly two types:

- Fixed Interest Rate

- Floating Interest Rate

Some lenders also offer a hybrid loan, which combines both.

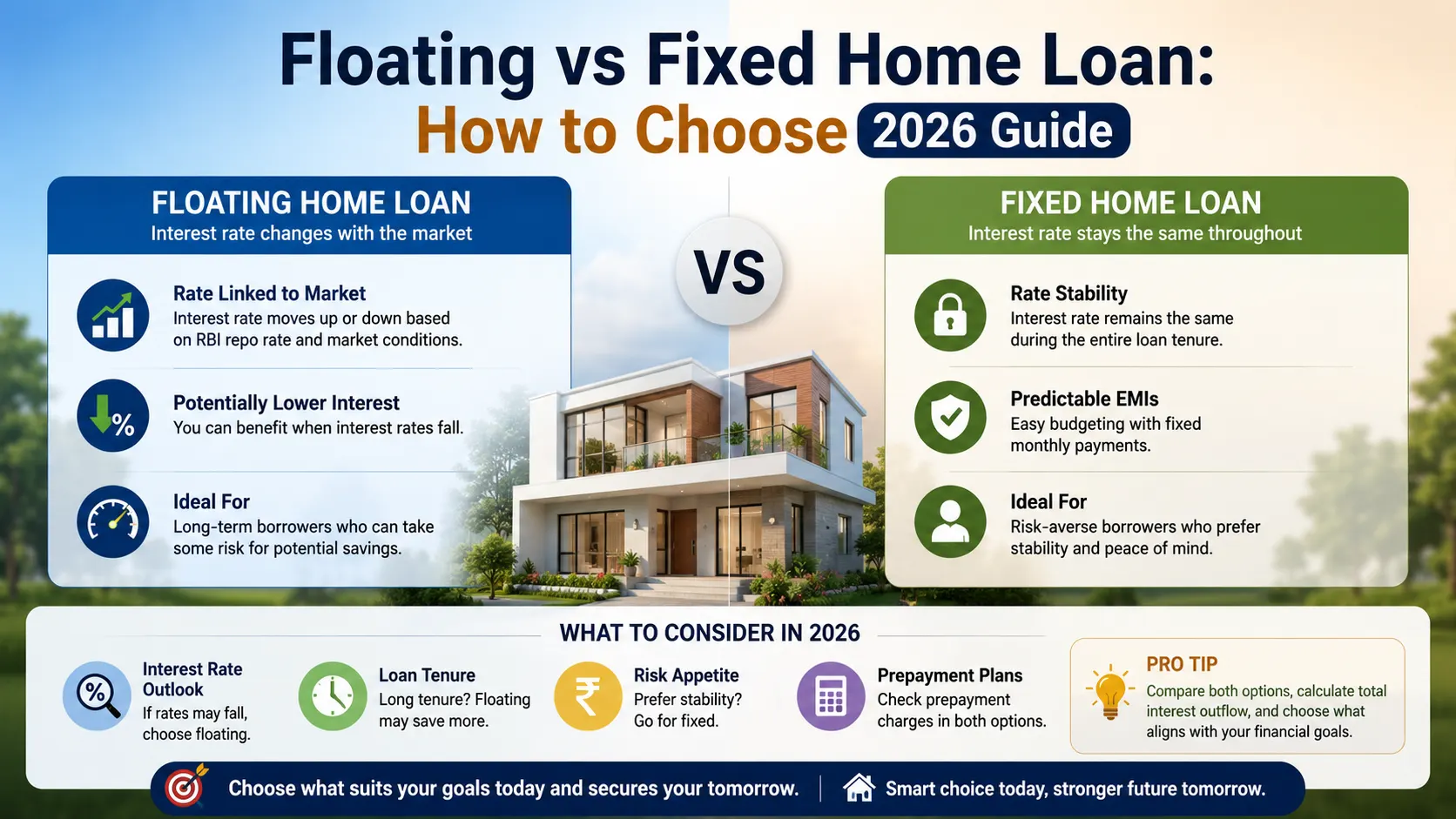

What Is a Fixed Home Loan?

A fixed-rate home loan keeps the interest rate constant for a predefined period or the entire tenure.

Example:

If your loan interest rate is fixed at 8.5%, it remains unchanged even if market rates increase or decrease.

Features of Fixed Home Loans

- EMI remains stable

- Better financial planning

- Protection from rising interest rates

- Usually slightly higher than floating rates initially

- Limited benefit if market interest rates fall

Advantages of Fixed Home Loans

1. Stable EMI Throughout the Tenure

Your monthly EMI does not fluctuate, making budgeting easier.

Ideal for:

- Salaried individuals

- First-time homebuyers

- Families with fixed monthly income

2. Protection Against RBI Rate Hikes

If the RBI increases repo rates, floating loan borrowers pay higher EMIs, but fixed-rate borrowers remain protected.

3. Better Financial Predictability

You can plan:

- Savings

- Investments

- Household expenses

- Long-term goals

- without worrying about changing EMIs.

4. Peace of Mind

Many borrowers prefer certainty over risk, especially during uncertain economic conditions.

Disadvantages of Fixed Home Loans

1. Higher Interest Rate

Fixed loans generally start at rates higher than floating loans.

Example:

- Floating: 8.25%

- Fixed: 8.85%

Even a 0.5% difference can significantly increase total repayment.

2. No Benefit When Interest Rates Fall

If market rates decrease:

- Floating borrowers enjoy lower EMIs

- Fixed borrowers continue paying the same rate

3. Prepayment Charges May Apply

Some banks impose penalties on early closure or refinancing.

4. Fixed May Not Stay Fully Fixed

In India, many “fixed” loans are actually fixed only for:

- 2 years

- 5 years

- 10 years

After that, they convert to floating.

Always read the loan agreement carefully.

What Is a Floating Home Loan?

A floating-rate home loan changes according to market interest rates.

The rate is usually linked to:

- RBI repo rate

- External benchmark lending rate (EBLR)

- Bank lending policies

If rates rise or fall, your EMI or tenure changes accordingly.

Features of Floating Home Loans

- Interest rates change over time

- Lower starting interest rate

- Benefit during falling interest cycles

- EMI or tenure may fluctuate

Advantages of Floating Home Loans

1. Lower Initial Interest Rates

Floating loans generally begin at lower rates than fixed loans.

This reduces the initial EMI burden.

2. Benefit When Interest Rates Fall

If RBI cuts repo rates:

- Your loan interest may reduce

- EMI may reduce

- Total interest payable decreases

This can save lakhs over long tenures.

3. Lower Overall Cost in Long Term

Historically in India, floating rates have often been cheaper over long periods.

4. No Prepayment Penalty

Most floating-rate home loans do not charge penalties for:

- Partial prepayment

- Full closure

This provides flexibility.

Disadvantages of Floating Home Loans

1. EMI Uncertainty

EMIs may increase unexpectedly if rates rise.

This affects monthly budgeting.

2. Total Interest May Increase

During prolonged high-interest cycles, total repayment becomes significantly higher.

3. Difficult Financial Planning

Variable EMIs create uncertainty for:

- Families

- Young professionals

- New homeowners

4. Stress During Rate Hikes

Frequent repo rate hikes can increase:

- EMI burden

- Loan tenure

- Financial pressure

Which Home Loan Is Better in 2026?

The answer depends on:

- Income stability

- Market conditions

- Risk appetite

- Loan tenure

- Financial goals

Choose a Fixed Home Loan If:

You should consider a fixed-rate loan when:

- You prefer stable EMIs

- Interest rates are expected to rise

- You have a tight monthly budget

- You are a first-time buyer

- You want predictable finances

Choose Floating Home Loan If:

Floating loans are suitable when:

- Interest rates may reduce

- You can handle EMI fluctuations

- You plan early repayment

- You want lower initial EMIs

- You have higher income flexibility

RBI Repo Rate Impact in 2026

In India, home loan interest rates are strongly influenced by RBI repo rate decisions.

When RBI:

- Increases repo rate → Home loan rates rise

- Reduces repo rate → Home loan rates fall

Floating-rate borrowers are directly affected.

Fixed-rate borrowers remain protected for the fixed period.

Should You Switch from Fixed to Floating?

You may consider switching if:

- Market rates are falling

- Your current fixed rate is very high

- The conversion fee is reasonable

Before switching, compare:

- Conversion charges

- Remaining tenure

- Total savings

- New EMI structure

Important Factors Before Choosing

1. Loan Tenure

Longer tenure = greater impact of interest fluctuations.

2. Income Stability

Unstable income may favor fixed rates.

3. Economic Conditions

Rising inflation often leads to higher interest rates.

4. Future Financial Goals

Consider:

- Marriage

- Education expenses

- Business plans

- Investments

5. Prepayment Plans

If you plan aggressive prepayment, floating loans are often better.

Expert Tips for Home Loan Borrowers in 2026

Compare Multiple Banks

Never choose the first offer.

Compare:

- Interest rate

- Processing fee

- Foreclosure terms

- Customer service

Maintain High Credit Score

A score above 750 improves chances of lower interest rates.

Negotiate with Banks

Many lenders offer better rates for:

- Salaried professionals

- Women borrowers

- Existing customers

Frequently Asked Questions

1. Which is cheaper: fixed or floating home loan?

Floating home loans are usually cheaper over long tenures if interest rates remain stable or decline.

2. Is floating home loan risky?

Floating loans carry interest-rate risk because EMIs can increase when market rates rise.

3. Can I switch from fixed to floating loan later?

Yes, most banks allow conversion by paying a conversion fee.

4. Which loan type is better during inflation?

Fixed-rate loans are generally safer during high inflation and rising interest cycles.

5. Do floating loans always reduce when RBI cuts rates?

Usually yes, but banks may adjust rates based on reset periods and lending policies.

6. What is a repo-linked home loan?

A repo-linked loan is tied directly to the RBI repo rate, causing faster interest rate changes.

7. Are fixed home loans truly fixed?

Not always. Many Indian banks offer fixed rates only for a limited period.

8. Can EMI increase in floating loans?

Yes. Banks may increase EMI or loan tenure when interest rates rise.

9. Which is better for first-time homebuyers?

Fixed loans are often better for buyers seeking predictable monthly payments.

10. Is prepayment free in floating home loans?

Most floating-rate home loans do not have prepayment penalties for individual borrowers.